Desk Report

Oniket Desk

Bangladesh enters the FY2026–27 budget cycle with an inflation crisis that is no longer cyclical, it is structural. Inflation reached 9.13 percent in February 2026 and remained above 8 percent for more than 41 consecutive months. Wage growth has lagged inflation for 47 consecutive months. For low and middle-income households, the arithmetic of daily survival has become grimly precise: food, rent, transportation, and electricity are consuming ever-larger shares of stagnant incomes, leaving nothing to save and increasingly little to spend.

The forthcoming budget must treat the cost of living not as a macroeconomic footnote but as the central social emergency it has become. It must address the structural mechanism most responsible for amplifying consumer prices at every level of the supply chain: the brokerage premium extracted by intermediaries between producer and consumer.

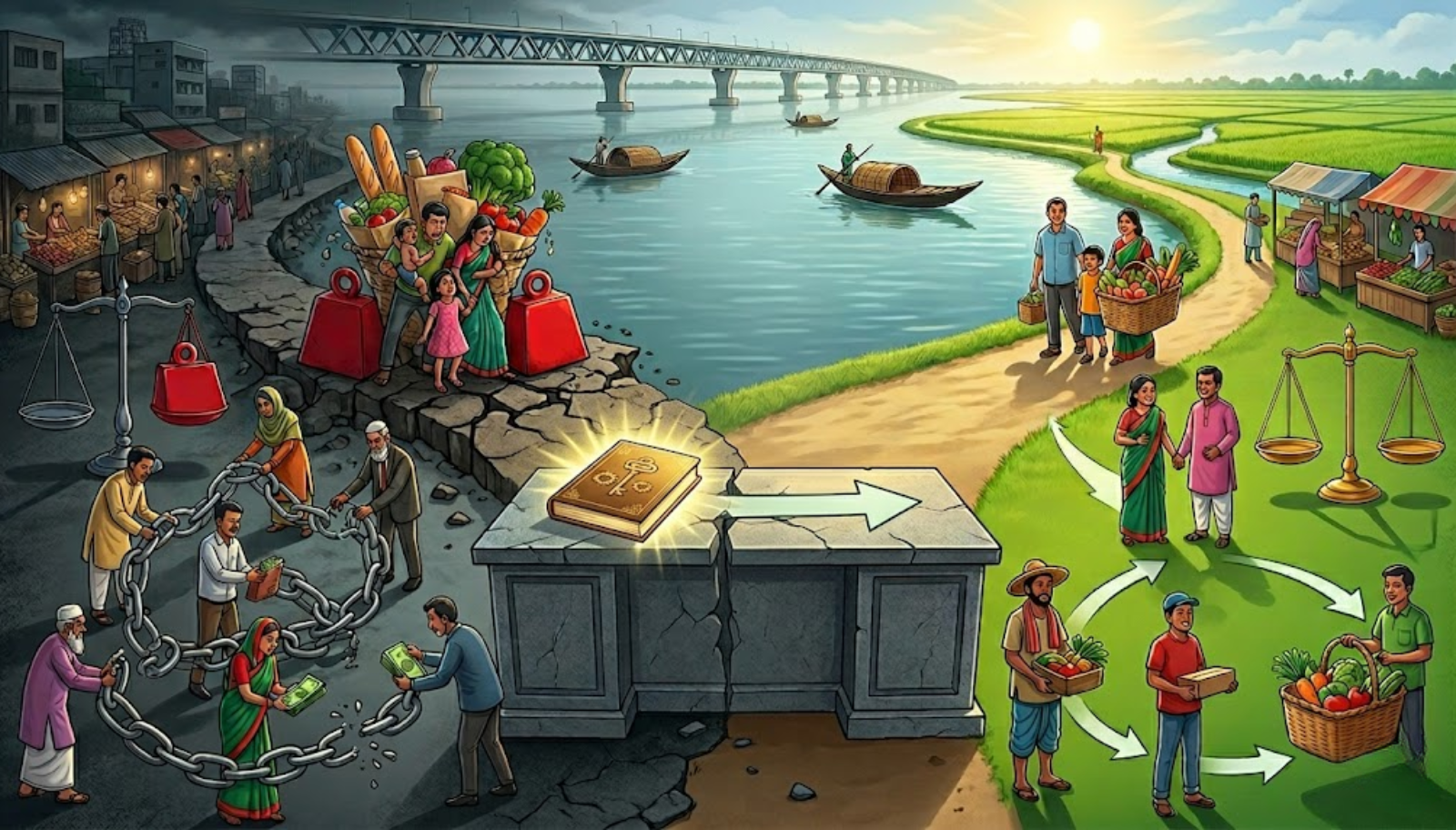

The Supply Chain Problem at the Core of Inflation

Bangladesh’s inflation is not primarily a monetary phenomenon. As the Centre for Policy Dialogue has explicitly noted, it is driven by supply-side bottlenecks, structural inefficiencies, and the entrenched role of middlemen and market syndicates who capture value at multiple points in the supply chain without adding commensurate productive contribution.

The evidence is visible in any Dhaka wholesale or retail market: falling international commodity prices do not translate into lower domestic prices because each link in the domestic chain, from assembler to wholesaler, aratdar to retailer, applies its own markup, often unchecked by regulation or competition. A vegetable that leaves a farm in Bogura at one price arrives on a Dhaka consumer’s table at a price two to three times higher, with the producer capturing a shrinking share and the intermediary layer capturing a growing one. This is not market efficiency; it is market capture, and the budget must respond to it as such.

What the Budget Must Directly Provide

The forthcoming budget must allocate dedicated resources to three immediate cost-of-living interventions. First, the Open Market Sale programme through which the Trading Corporation of Bangladesh sells essential commodities at subsidised prices must be significantly expanded in geographic coverage and product range, reaching urban peripheries and rural markets that current distribution networks do not serve.

Second, targeted transport subsidies for essential commodity logistics must be introduced, directly reducing the freight cost component that retailers use to justify price escalation.

Third, the budget must fund a meaningful expansion of public cold storage capacity linked to production clusters in key agricultural districts, reducing the post-harvest losses and artificial scarcity that syndicates exploit to sustain inflated prices.

Structural Reforms to Cut Brokerage Premiums

Beyond direct budget allocations, the budget must signal and fund a set of structural reforms that dismantle the intermediary premium architecture. A digitally integrated agricultural marketplace connecting registered farmers directly to institutional buyers, supermarkets, and export processors must receive dedicated capitalisation. Pilot farmer-to-consumer direct market channels, already proven in limited contexts, must be scaled into a national programme with infrastructure, logistics support, and price transparency mechanisms.

Intermediary margin regulation that establishes legal maximum markup thresholds at each identifiable point in designated commodity supply chains must be legislated and enforced through a resourced Consumer Rights Protection Directorate, whose current monitoring capacity is demonstrably inadequate.

Market syndicate prosecution must be treated as a fiscal priority, not merely a law enforcement matter. The Competition Commission of Bangladesh must receive the institutional resources and political mandate to investigate and penalise collusive pricing behaviour systematically. The budget should fund dedicated market intelligence units within the Ministry of Commerce to track price formation in real time and trigger enforcement responses before artificial shortages harden into prolonged consumer harm.

The Fiscal and Social Imperative

The cost-of-living crisis in Bangladesh is not an external shock that monetary policy alone can absorb. It is a governance failure embedded in the architecture of markets that have been allowed to operate without effective competition, transparency, or accountability. The FY2026–27 budget has both the opportunity and the obligation to treat supply chain reform not as a technical afterthought but as a first order fiscal and social priority. Until the brokerage premium is structurally reduced, no level of subsidy, open market sale, or monetary tightening will deliver sustained relief to the households who need it most.